During the financial crisis of 2008, I started to figure out just how important the psychology of personal finance was compared to the math. The numbers and math are simple. If you save 10-15% of your income, and invest it for 40 years in a boring index fund you will end up with a pile of money at 65 to comfortably retire. So why is this so hard? Why do people not have more money saved for retirement? The simple answer is we are our own worst enemy:

We don’t prioritize saving enough and get caught up in the consumerism of keeping up with the Joneses

We try and time the market

We buy high and sell low in a panic

We don’t know how to evaluate risk

We listen to all the media that have advocated and pushed this for decades. I am looking at you CNBC.

While my awareness to the mental aspects of personal finance started in 2008, it still took me a few more years to realize that dollar cost averaging was the single best way to fight and win against the psychology of money.

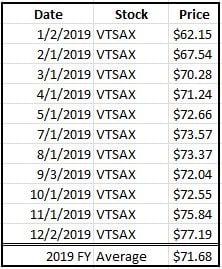

Like many things I write about, this concept is not complex or difficult to understand. Dollar cost averaging is an investment strategy where you buy shares over a period of time and the number of shares acquired fluctuates depending on the price at the time of purchase. In practical terms, a $500 investment each month in your Roth IRA is an example of dollar cost averaging. The same concept applies to your paycheck deductions for things like your 401k or HSA. You are making investments over a period of time and are continually investing regardless of the direction of the market.

This last statement is why dollar cost averaging is so powerful for personal finance. You no longer care which direction the market is going. If the market is up, GREAT my assets are appreciating, if the market is down, GREAT I am buying in when the market is on sale! I can’t tell you how liberating this concept is and how it changed my entire mental state regarding my personal finance invstments. I no longer worry about when to buy, since it happens automatically every two weeks! When you combine dollar cost averaging, with my 100% VTSAX investment strategy, you have a powerful system to achieve financial independance.

I want to emphasize that there is a lot of well respected research that suggests that lump sum investing is actually better in the long run than dollar cost averaging. My counter argument to this is that personal finance has never actually been about the numbers, it is about human behavior! So yes, lump sum investing may lead to higher theoretical returns dollar cost averaging is still a powerful tool. If you are deciding what to do with a windfall or inheritance that is a different story, and depending on your own situation and risk tolerance levels, you may prefer to put it all in at once. For me, I will continue on the slow, steady, and boring path of dollar cost averaging VTSAX to financial independence.

A search on Amazon for “Investing” returns 40,000 books on the topic. There is no shortage of books, opinions, or information written on investing. For the new investor, it is an intimidating topic that can seem somewhat overwhelming. I have conversations with many people who think investing is too complicated, or they are paralyzed by the fear of making a mistake. We have been tricked to believe that investing is a complex and difficult subject, one that is better left to the professionals on Wall Street. My goal here is to break this topic into 3 simple steps that create a road map for the average investor. These steps will not cover every scenario or personal situation, but I truly believe that for 99% of people this is the simplest path to investing, growing wealth and becoming financially independent.

Step 1: Saving to Invest

This is often an overlooked step, but you can’t invest money if you don’t have anything left at the end of the month and are saddled with debt. To create a situation where you have the money to invest, you must spend less than you make, by creating and sticking to a monthly budget. Once you are generating savings at the end of each month, you are now ready to begin what I call “The Investment Walk”.

I believe there is a very specific path you should take when it comes to investing and deciding on where and how to invest your savings. I am not talking about investment allocations between stocks and bonds, or even what kind of financial instrument you should buy. I am talking about the programs and accounts you have available to invest in: 401k’s, Roth IRA’s, IRA’s, brokerage accounts etc. Here is the path laid out one brick at a time:

Have an emergency fund with 6 months of expenses. Life happens. An emergency fund is to help smooth out the unexpected that will inevitably happen. Having funds tucked away in an online savings account like Ally Bank, will help prevent these events from derailing your investment walk.

Be debt free except for your house. I have always had an aversion to debt. It is simply how I am wired, and it has served me well over the years. The only acceptable debt I believe you should carry is a mortgage on your primary residence. Get rid of all other debts, and you are truly ready to make your first investment.

Fund your 401k up to your employer match. Many employers will offer a 401k (or simmilar) savings plan along with a company match. Participating in a 401k, up to your employer match, equates to a guaranteed 100% return on your investment. You won’t find anything that provides better returns than this! If your employer offers a 401k match, you are literally leaving free money on the table if you don’t take advantage of this. It blows my mind, the number of people I see in my job not participating in the company matched 401k’s.

Fund your Roth IRA up to the maximum allowed. The Roth IRA is a fantastic retirement vehicle. Unlike your 401k, which is taken out pre-tax, the Roth IRA contribution is done with after tax dollars. While this might initially be seen as a negative, the huge benefit of the Roth IRA is that withdrawals are tax free and there are no minimum required distributions! If you contribute to a Roth IRA early in your career, you can build a sizable tax free nest egg. Maximum contributions for 2020 are $6,000. The only downside to the Roth IRA is that is is not available to individuals making over $139k or married couples making over $206k per year. Learn more

Fund your remaining 401k up to the maximum allowed. If you have completed steps 1-4 you are really starting to make some progress on your long term retirement goals! If you still have funds left we go back to the 401k and fund the remainder up to the maximum which is $19,500 in 2020.

Fund your Health Savings Account (HSA) to the maximum. If you participate in a high deductible health plan, you can contribute $7,100 in 2020 to an HSA pre-tax for future medical expenses. Leveraging this benefit is a great hedge against rising healthcare costs. Read more about why I love Health Savings Accounts.

If you have kids, contribute to a 529 college savings plan. College is expensive, but the 529 savings plan allows for tax free investment growth to help pay for college

Pay down your mortgage until it is paid off. There is probably no topic in the personal finance community that is debated more than paying off your mortgage. There are some that are strongly for it and there are just as many that are against it. For me, I simply don’t like debt of any kind, and recommend paying off your mortgage.

Invest in a taxable Vanguard brokerage account. If you have made it this far, you are a personal finance rock star. You have a strong income, you are spending significantly less than you make, and you have just paid off your house! What next? Now you can take your mortgage payment and start investing that each month!

Step 3: Investment Allocations

After laying out the investment path above, we now need to turn to the allocation side of investing. What are we actually going to invest in? Are we going to buy stocks, bonds, or mutual funds? This step is where I see people struggle the most and where most bad decisions are made. The good news is that I am going to make this super simple!

As much as I love VTSAX, unfortunately not every account provider is going to offer it, however, most should offer something similar. Here are our current accounts and how they are invested:

Since we have a long time horizon, we are 100% invested in low cost, broad market, index funds!

What if you are closer to retirement?

If you are closer to retirement, or if you just want to adjust your risk profile you can always add the Vanguard Total Bond Market Index Fund (VBTLX) to your portfolio. With just these two funds, VTSAX and VBTLX, you can easily control your investing approach and risk tolerance. It does not get any easier than that!

With these three simple concepts, combined with my investment walk, you can start down the path of growing wealth and achieving your financial goals.